A Compliance Newsletter by: The Baldwin Regulatory Compliance Collaborative (BRCC)

Welcome to the June 2023 issue of the Baldwin Bulletin – a monthly guide to important legal news and employee benefits-related industry happenings, designed to keep you abreast of the latest developments.

This month’s issue of the Baldwin Bulletin focuses on providing employers with important 2023 compliance deadlines, as well as certain compliance issues that potentially will have a significant impact on employers over the next several months.

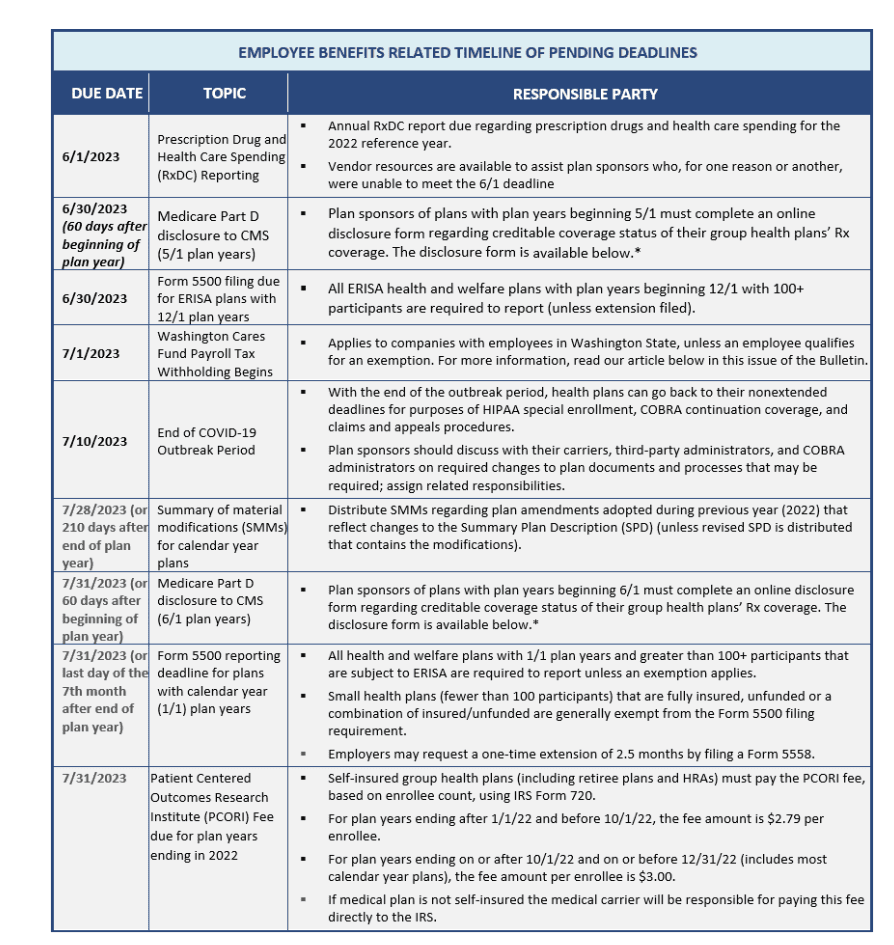

Upcoming 2023 Compliance Deadlines

Employers must comply with numerous reporting and disclosure requirements throughout the year in connection with their group health plans. The attached Compliance Timeline explains key compliance deadlines for employer-sponsored group health plans for the remainder of the year. Please note the following upcoming deadlines:

*https://www.cms.gov/Medicare/Prescription-Drug-Coverage/CreditableCoverage/CCDisclosureForm.html

Outbreak Period Set to End

On April 10, 2023, President Biden signed a joint resolution ending the COVID-19 national emergency that had been in place since early 2020. Although President Biden signed the resolution ending the national emergency declaration on April 10, the Departments of Labor (DOL), Health and Human Services (HHS) and the U.S. Treasury (collectively, the Departments) have informally indicated that the May 11, 2023, date announced in FAQs Part 58 represents the end of the national emergency for purposes of ending the outbreak period 60 days later, on July 10, 2023.

Employer Action Items

Please review our previously issued Alert, containing helpful employer action steps, along with three tables of action items to assist employers with the end of the public health emergency (PHE), national emergency, and outbreak periods. Note that the Alert was issued prior to President Biden’s announcement, and like FAQ, Part 58, assumes a May 11, 2023, end-date for the termination of the national emergency and corresponding end to the outbreak period on July 10, 2023.

More Information

As part of the April 10th announcement, the Department of Labor provided additional guidance on the end of the COVID-19 public health emergency and national emergency, including:

- Tips for employers and health plan sponsors

- Five ways the end of the public health emergency could affect your health coverage

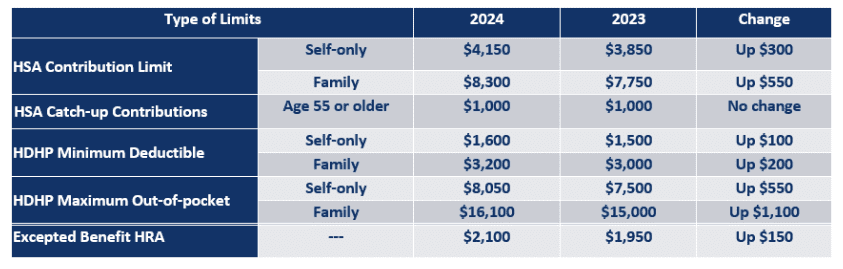

IRS Announces 2024 HSA/High Deductible Health Plan Limits

The Internal Revenue Service (IRS) has released Revenue Procedure 2023-23 to provide the inflation-adjusted limits for health savings accounts (HSAs) and high deductible health plans (HDHPs) for 2024, as well as the maximum contribution amount that can be made by an employer to an excepted benefit HRA for plan years beginning in 2024.

These limits vary based on whether an individual has self-only or family coverage under an HDHP and include:

- The maximum HSA contribution limits effective January 1, 2024;

- The minimum deductible amount for HDHPs for 2024 (Note: higher minimum deductible amounts may apply for California and other state insurance policies to comply with state law requirements);

- The maximum out-of-pocket expense limit for HDHPs for 2024

Employer Action Items

Employers that sponsor HDHPs should review their plan’s cost-sharing limits (minimum deductibles and maximum out-of-pocket expense limits) when preparing for the plan year beginning in 2024.

Also, employers that allow employees to make pre-tax HSA contributions should update their plan communications for the increased contribution limits.

Summary

The following chart shows the HSA/HDHP and Excepted Benefit HRA limits for 2024 as compared to 2023:

More Information

Revenue Procedure 2023-23 is available here.

PCORI Fee Payment Reminder

The annual fee to fund the Patient-Centered Outcomes Research Institute (PCORI) is due on July 31, 2023. The fee is paid by filing IRS Form 720 (Quarterly Federal Excise Tax Return) and is based on the number of “covered lives” during the plan year. The fee per covered life depends on the plan year end date, as follows:

Plan year ended during: Fee per covered life:

January 1, 2022 – September 30, 2022 $2.79

October 1, 2022 – December 31, 2022 $3.00

Employer Action Items

Plan sponsors of self-insured plans are responsible for paying the annual fee. In this respect, they should consider the following:

- Determine self-insured health plans (including level funded plans and HRAs integrated with fully insured medical plans).

- Calculate the PCORI fee using one of three permitted methods (described below).

- For health reimbursement accounts (HRAs) integrated with fully insured medical plans, calculate separate fee.

- Maintain records documenting the calculation and payment to substantiate enrollment count and method used.

For plan sponsors of fully insured plans, the PCORI fee is generally payable by the insurance companies, thus no action is required on their part unless responsibility to do so has been transferred to them by the insurer.

One of the following methodologies may be used for determining the average number of covered lives under the plan for the plan year:

- The Actual Count Method. Under the Actual Count Method, the average number of covered lives is determined by adding the totals of lives covered each day of the plan year and dividing by 365 or 366, as applicable.

- The Snapshot Method. Under the Snapshot Method, the average number of covered lives is based on the total number of covered lives on a particular date (or dates) in the first, second, or third month of each quarter, divided by the number of dates on which the count was made. An equal number of dates must be used for each quarter, and each date used must be within three days of the corresponding date in the other quarters under this method.

- The Form 5500 Method. Under the Form 5500 Method, for a plan that offers both self-only coverage and dependent (family) coverage, the average number of covered lives is based on the total number of participants covered at the beginning and the end of the plan year divided by two, per the Form 5500 (or Form 5500-SF) that was filed for the plan no later than July 31 following the end of the plan year being reported on.

Background

The PCORI was established as the result of the Affordable Care Act (ACA). It is a nonprofit corporation designed to assist patients, clinicians, purchasers, and policymakers in making informed health decisions by advancing the quality and relevance of evidence-based medicine through the synthesis and dissemination of comparative clinical effectiveness research findings.

The annual PCORI fee is considered an excise tax that must be reported on IRS Form 720 for the second-quarter reporting period. It is due by July 31 of the year following the last day of the plan year being reported on. Payment is to be remitted along with the Form 720 filing, and the amount will vary depending on the plan year. Employers who sponsor self-insured plans are responsible for paying this fee, as are insurers of most fully insured policies.

Plans subject to the PCORI fee include plans sponsored by private employers, state and local governmental health plans, both grandfathered and non-grandfathered plans, retiree-only medical plans, HRAs, and health care flexible spending accounts (FSA) that are not excepted benefits under HIPAA. The fee is not assessed against excepted benefits under HIPAA, such as stand-alone dental and vision plans and most health care FSAs, as well as employee assistance, disease management, and wellness programs not providing significant medical care benefits, plans covering primarily employees working outside the United States, and stop-loss and reinsurance policies.

A plan sponsor is also able to treat multiple self-insured plans with the same plan year as a single plan for reporting and payment purposes. For example, a plan sponsor with a self-insured plan providing major medical benefits and a separate self-insured plan with the same plan year that provides prescription drug coverage may be considered as a single plan so that the same covered life under each plan is counted only once. Note, however, plan sponsors that have established a health reimbursement account (HRA) integrated with their fully insured medical plan may be subject to a separate PCORI fee assessment for that HRA.

More Information

For further information, including links to the final PCORI regulations, questions and answers regarding the PCORI Fee, a chart depicting the types of insurance coverage subject to the fee, and the Form 720, along with instructions, please visit the IRS website here.

IRS Issues Guidance on FSA Substantiation Requirements

The IRS recently issued a Chief Counsel Advice Memorandum that provides important reminders about the claims substantiation requirements for flexible spending accounts (FSAs). These requirements apply to FSAs that reimburse medical expenses (health care FSAs) and FSAs that reimburse dependent care expenses (dependent care FSAs).

Employer Action Items

Reimbursements from FSAs that are not fully substantiated must be included in the employee’s gross income. Also, if a Section 125 cafeteria plan does not comply with the substantiation requirements for FSAs, the plan will no longer qualify for favorable tax benefits. To avoid these negative tax consequences, employers with FSAs should review their substantiation procedures to make sure they comply with IRS rules. Likewise, those employers who engage a third-party administrator should confirm their compliance with these requirements.

Summary

Most FSAs are offered under a Section 125 cafeteria plan to allow employees to make pre-tax contributions. Under federal tax rules, all claims for reimbursement from an FSA must be substantiated by information from a third party that is independent of the employee and the employee’s spouse and dependents, such as an explanation of benefits (EOB) from an insurance company or a detailed receipt from a medical or dependent care provider.

Many FSAs use debit cards to make it easier for participants to access their funds. Certain electronic transactions qualify for automatic substantiation, which means that employees are not required to submit additional information following the transaction (i.e., certain recurring medical expenses incurred at certain providers that match the amount, medical care provider, and the time-period of previously approved expenses).

Specifically, according to the IRS memorandum, the following methods are not permissible for substantiating reimbursements of medical expenses from an FSA:

- Allowing employees to self-substantiate expenses.

- Requiring substantiation of only a random sample of unsubstantiated charges to the debit card (that is, charges that are not automatically substantiated).

- Not requiring substantiation for debit card charges that are less than a specified dollar amount.

- Not requiring substantiation for debit card charges from certain dentists, doctors, hospitals or other favored health care providers.

- Dependent care expenses may not be reimbursed before the date the expenses are incurred. Dependent care expenses are considered incurred on the date the care is provided and not when the employee is formally billed or charged for (or pays for) the dependent care.

More Information

The IRS Counsel Advice Memorandum is available here.

Sun Life Report Provides Insights Into Self-Insured Plan Expenses

In the 2023 edition of its “High-cost Claims and Injectable Drug Trends Analysis” report, Sun Life Assurance Company of Canada (Sun Life), a life and disability insurance company, found that in the past year, million-dollar claims per million covered employees increased by 15%, and 45% from 2019 to 2022. In fact, 20% of employers had at least one member with over $1 million in claims during the four-year benefit period from 2018 through 2021. Sun Life has analyzed its claims data for the past eleven years to assist self-insured employers in understanding the trends and potential impacts of highest-cost medical and injectable drug claims.

Employer Action Items (Sponsors of Self-insured Plans)

- Stay up to date on current stop-loss trends – such as reviewing the Sun Life report (link available below)– and understanding the potential impacts of high-cost medical and drug claims in order to take steps to better support the health of employees and better protect themselves against rising health care costs.

- Work with your benefits broker to design and implement effective strategies to manage rising health care costs.

- Consider implementing options for improving health care affordability.

- Assess ways to reduce the risk of high-cost and catastrophic claims.

Summary

This report analyzed claims data from 2019 to 2022, representing more than 55,000 members, over $5.5 billion in total stop-loss reimbursements and $12.2 billion in total costs. This data set includes the full Sun Life stop-loss book of business.

Key Findings

- The report found that 71% of all stop-loss claims came from the top 10 high-cost conditions, with cancer being the highest at $324.8 million in reimbursements. The top 10 ranking conditions for 2022 were as follows:

- Malignant Neoplasm (another term for a cancerous tumor).

- Cardiovascular.

- Leukemia, lymphoma and multiple myeloma.

- Orthopedics and musculoskeletal conditions.

- Newborn and infant care.

- Sepsis.

- Gastrointestinal conditions.

- Neurological conditions.

- Respiratory conditions.

- Urinary and renal conditions.

- 11 of the top 20 high-cost injectable drugs were related to treating cancer, with the new cancer drug Rylaze having the highest average cost in 2022 at $808,700.

- Cardiovascular disease jumped from the third-highest claim to the second in 2022, with $142.4 million in reimbursements.

- Notably, Sun Life indicated that they are seeing greater consistency in both the top 10 and top 20 high-cost conditions; however, there are also significant changes within and beyond their top claim conditions.

- Nearly 1 in 9 employers (11%) had a birth-related stop-loss claim from 2018 through 2021. Additionally, the preterm birth rate increased by 10.5% from 2020 to 2021. In 2022, newborn and infant care ranked fifth among the highest-cost claim conditions, with an average cost of $371,800. The report highlights that while fewer members in employer self-insured plans make preterm or infant care claims, the costs of pediatric care, such as required specialty care at children’s hospitals, caused its high ranking.

More Information

Click here to read the full report from Sun Life.

Payroll Tax Withholding for Washington Cares Fund To Begin July 1, 2023

Payroll tax withholding under the Washington Long Term Care Act will begin on July 1, 2023, for companies with employees in Washington State, unless an employee qualifies for an exemption. As such, employers need to not only prepare themselves to withhold that tax, but also identify those employees who are exempt from the withholding.

Employer Action Items

- Review the WA Cares Toolkit Calendar. The toolkit includes long content that can be used for months through July, short content and graphics covering a range of topics, videos and designed materials, and frequently asked questions (FAQs).

- Proactively communicate with employees about WA Cares- early and often. Workers often look to their employers for guidance as their most direct and trusted source of information. Furthermore, communication is more effective when sending as a stand-alone message versus as part of a broader communication piece.

- The content of the communications should include information on the benefit, not just the contribution requirement. To fully understand the program, they are paying into, workers need to get information on how to qualify for the benefit and what services the benefit can be used to pay for. In addition, consider including a reminder to employees that if they want to apply for an exemption, they should do so as soon as possible considering the upcoming payroll tax withholding.

- Provide resources to managers as well as all Human Resources and payroll professionals as they are most likely to be approached by employees with questions. These groups of staff need to be able to answer questions and point employees to more information.

Background

On May 13, 2019, Washington became the first state in the nation to establish a state-operated public insurance program to pay for long-term care services, to be funded solely through employee payroll assessments. Unlike private long-term care insurance, which requires premiums even after retirement, contributions to the fund will only be made while an individual is working and stop when work stops.

On January 27, 2022, the Washington Legislature and Governor Inslee announced reforms to address coverage gaps and delay program implementation by 18 months. Workers who did not receive an exemption, will now begin contributing to the WA Cares Fund on July 1, 2023. These workers can earn a maximum of $36,500 in lifetime long-term care insurance (adjusted annually for inflation) by contributing 0.58% of their wages in premiums while they are working.

More Information

For more information, please visit the WA Cares Fund website. For questions about how to use the toolkit or to request additional materials, contact wacaresfund@dshs.wa.gov. Please include “toolkit” in your subject line.

Question of the Month

Question: Is a telehealth benefit subject to ERISA?

Answer: The general rule is yes to the extent that the benefit is sponsored by a private sector employer. These benefits are often offered under an employer’s group health plan. However, even if telehealth benefits are offered separately from the employer’s group health plan, the benefits are likely subject to ERISA.

There is an exception available under a Department of Labor (DOL) regulatory safe harbor that allows certain group insurance arrangements with minimal employer involvement to be exempt from ERISA even if they provide ERISA-listed benefits. In general, to be exempt from ERISA, the arrangement must be a voluntary employee-pay-all telehealth benefit offered by a third party, with very limited employer involvement. Otherwise, it must comply with ERISA’s rules, such as having a plan administrator, claim and appeal procedures, a summary plan description, and potential reporting requirements.

In addition to ERISA, there are other considerations, including those under COBRA, HIPAA, and coverage mandates such as first-dollar coverage of preventive services, not imposing annual or lifetime dollar limits on essential health benefits, and parity in mental health and substance use disorder benefits.

Moreover, telehealth coverage may affect an individual’s ability to contribute to a health savings account (HSA), although temporary relief provides that telehealth and other remote care services provided on or after January 1, 2020, will not cause a loss of HSA eligibility for plan years beginning on or before December 31, 2021; for months beginning after March 31, 2022, and before January 1, 2023; and for plan years beginning after December 31, 2022, and before January 1, 2025.

Source: Thompson Reuters

Comments are closed.